2024-01-26

Katharine Graham had a very unusual way of taking the helm at the Washington Post. Her father, Eugene Graham, had founded the Washington Post, and in 1946, he asked his daughter's husband, Philip Graham, a Harvard-trained lawyer, to run the company. After his death by suicide in 1963, Katharine Graham assumed the role of CEO. Despite being shy, having never been fully employed for the last 29 years and four kids.

The Washington Post owned many companies, including the Post itself, Newsweek magazine, and television stations in Florida and Texas.

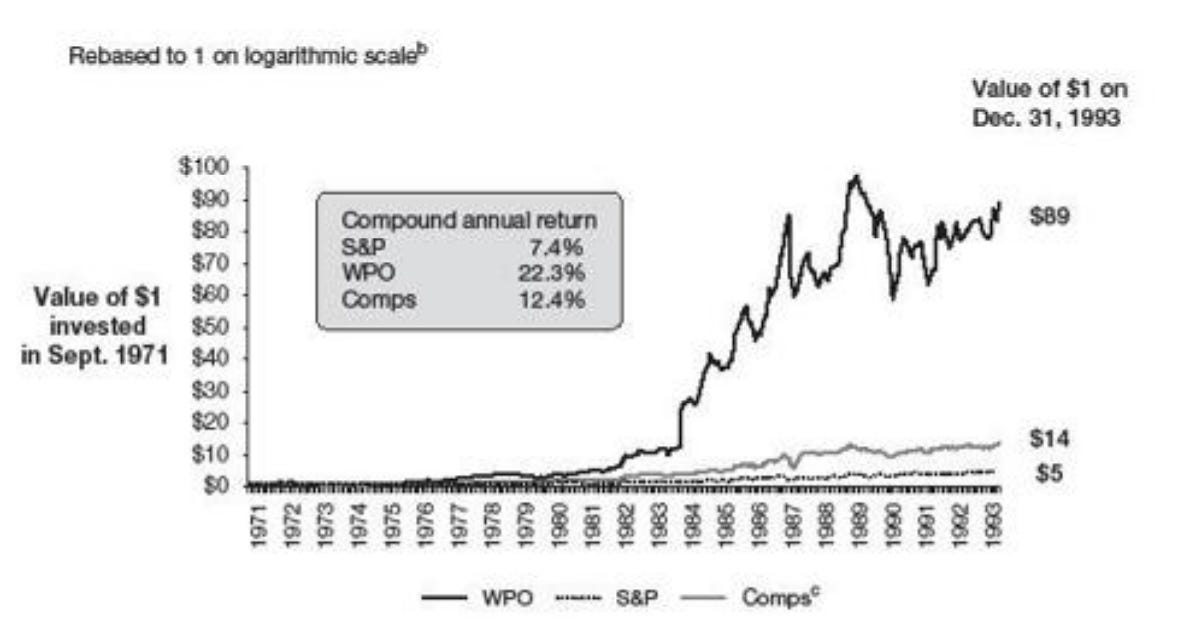

After several years of getting comfortable in her positions, she IPOed in 1971, where she raised $16 million. She also was not scared of publishing controversial articles, such as the internal Pentagon assessment of the war in Vietnam or the Watergate scandal.

She started to acquire the Trenton Times, which turned out to be a mediocre acquisition where she was not selective enough. In 1974, Warren Buffett started to acquire a 13% stake in the Washington Post and gained a seat on the board while advising her on strikes in her printing facilities and buying back stock (40% over the next years).

In the '80s, she further improved margins, while other competitors went out of business. She announced a compensation structure that emphasized competition and bonus payments. Additionally, she only made two acquisitions in that decade, which was contrary to her peers:

In '88, she sold the company's telephone assets for $197 million due to a large capital expenditure required to further maintain this business. In the '90s bear market, when everybody had too much debt due to prior acquisitions, she started to take advantage of these low prices by buying more businesses. In 1993, she stepped down as CEO and gave this title to her son.

Sources of Capital:

Alan Spoon stated, "The system was totally federalized, with all excess cash sent to corporate. Managers had to make the case for all capital projects. The key question was, 'Where's the next dollar best applied?' And the company was rigorous and skeptical in answering that question."

McKinsey advised to stop buybacks, which they overrode two years later – "most expensive consulting assignment ever!"

The new CEO, Donald Graham, made selected acquisitions, opportunistically repurchased stock (20%), and kept dividends low. Meanwhile, competitors like The New York Times overpaid for acquisitions, built a huge headquarters, and lost 90% of its stock value. Checkout the book The Outsiders for more Information

Thanks,

Finn